![]()

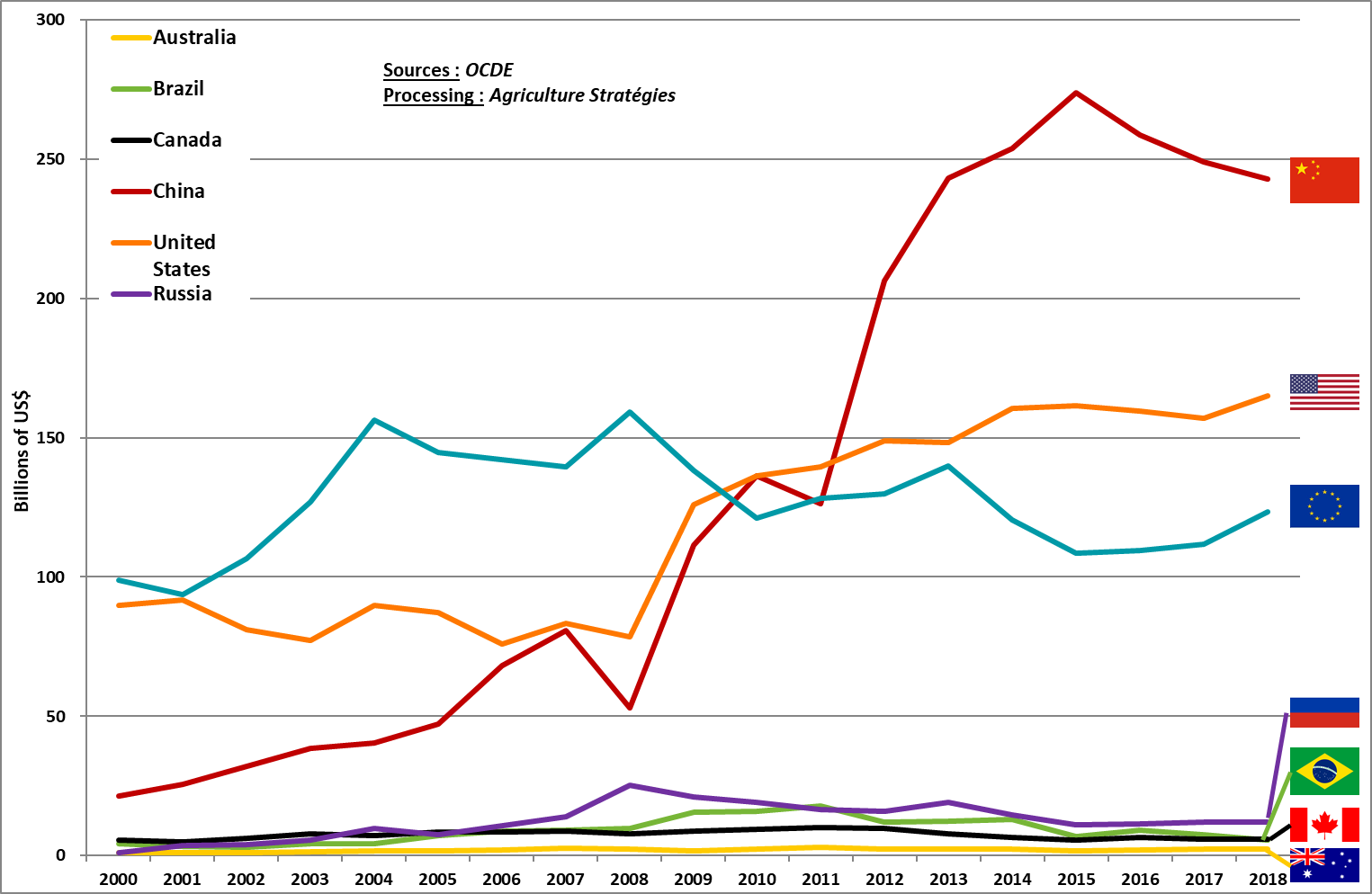

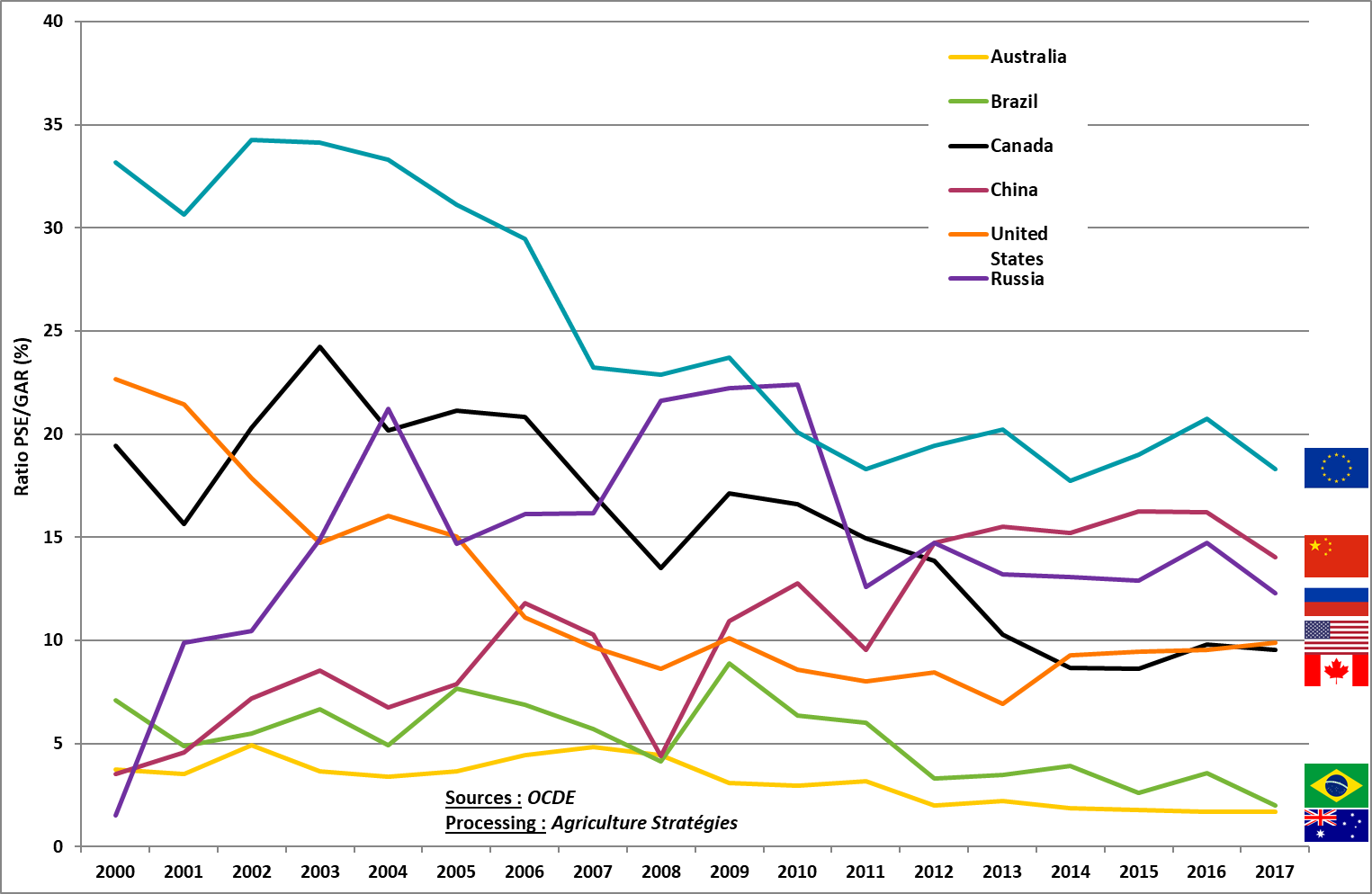

Total Support Estimate (TSE) collects all direct and indirect support for agriculture and food. It is broken down into two sub-indicators: Producer Support Estimate (PSE) and Consumer Support Estimate (ESC). Money subsidies are counted, but so are the measures taken to keep prices above international prices, which are generally very low – dumped prices – because they come close to the costs of production on the pioneer fronts of the producers. more competitive export, but whose production remains insufficient to meet all demand. The evaluation of these measures according to this logic is therefore questionable and we have already underlined it: rather than taking as a reference the observed international price, a real evaluation of the supports should be established starting from an estimation of the “normal” price. that is to say, the price corresponding to the production costs of the least competitive producers but nevertheless necessary to meet all needs. But in order not to bias the comparisons resulting from these indicators, we have not adjusted them at this stage. On the other hand, we have made indispensable adjustments, such as the reinstatement of a significant share of food aid in the US, which has been overshadowed by the OECD. In fact, only $ 34 billion is matched in the US ESC, while the budgetary cost of programs (Supplemental Nutrition Assistance Program, Scholl Breakfast Program, National Special Program Milk Program, Child / Adult Care Food Program, WIC etc.) amount to $ 101 billion a year (USDA source) over the 2014-2018 period. Figure 1: Evolution of Total Support Estimate (TSE) for Major Producing Countries Figure 1 shows the evolution since 2000 of the TSE for the 7 main agricultural powers: Australia, Brazil, Canada, China, the United States, Russia and the European Union. The United States (+ 80%), China (+ 853%) and Russia (+ 225%) experienced a significant increase in TSE over the period. This development was particularly noticeable between 2007 and 2012 under the double effect of the food crisis and the financial crisis that led these countries to strengthen their support for the development of agriculture and measures that favor the poorest populations. Beyond the absolute value of the EUT, it is useful to report this indicator of other quantities to account for differences in population, wealth or production.

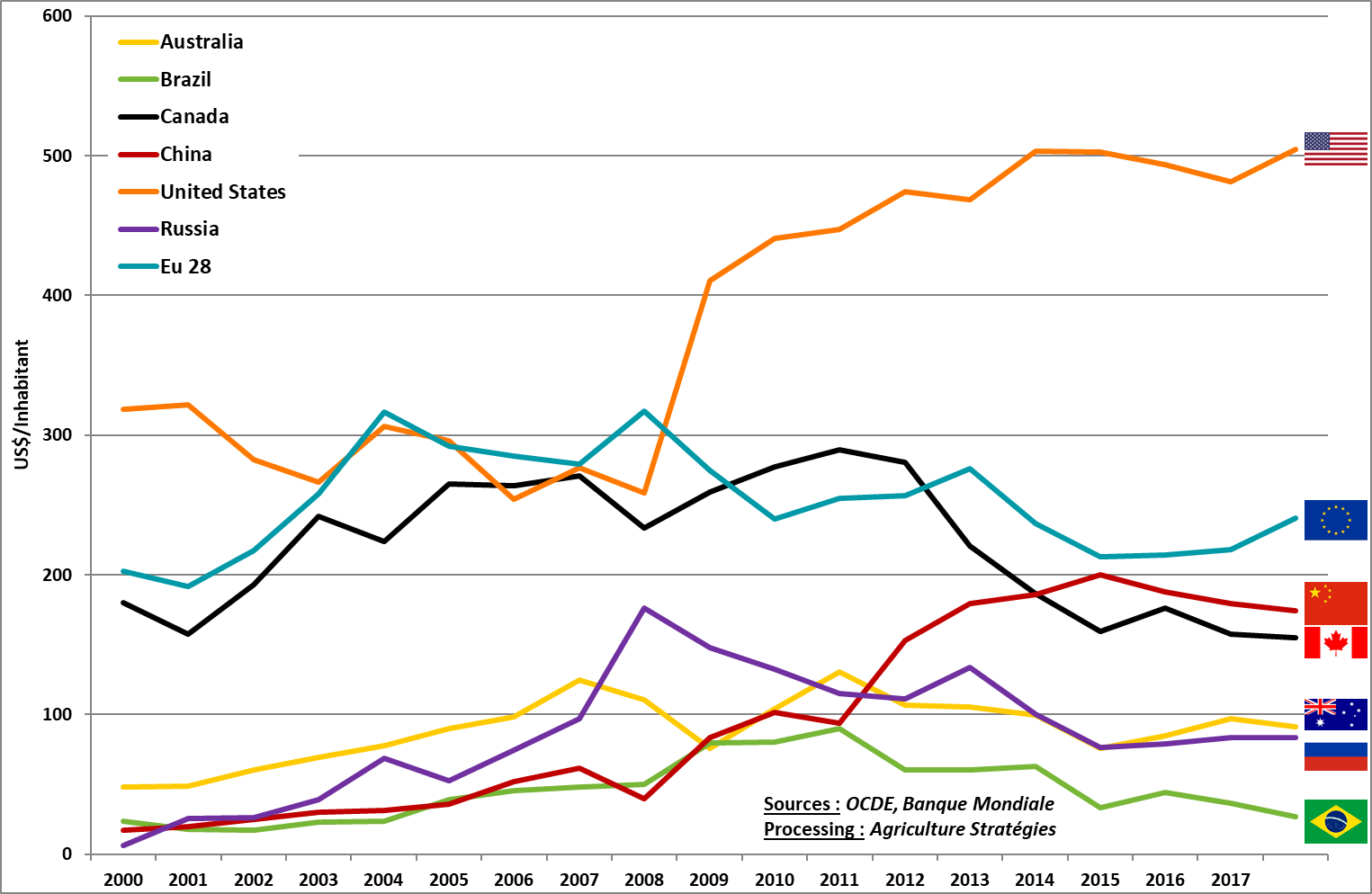

Figure 2 shows the TSE in relation to the number of inhabitants of the country concerned. Figure 2: Evolution of TSE per capita for the main producing countries With its 1.4 billion inhabitants, China is the most populous country. While the increase in the ratio of EST per capita remains apparent, China occupies only the third place at the end of the period with a TSE of $ 175 per inhabitant, a level close to the European Union ($ 240) and Canada ($ 155). ), a country with a much higher standard of living. With nearly $ 500 per capita, the United States is largely ahead.

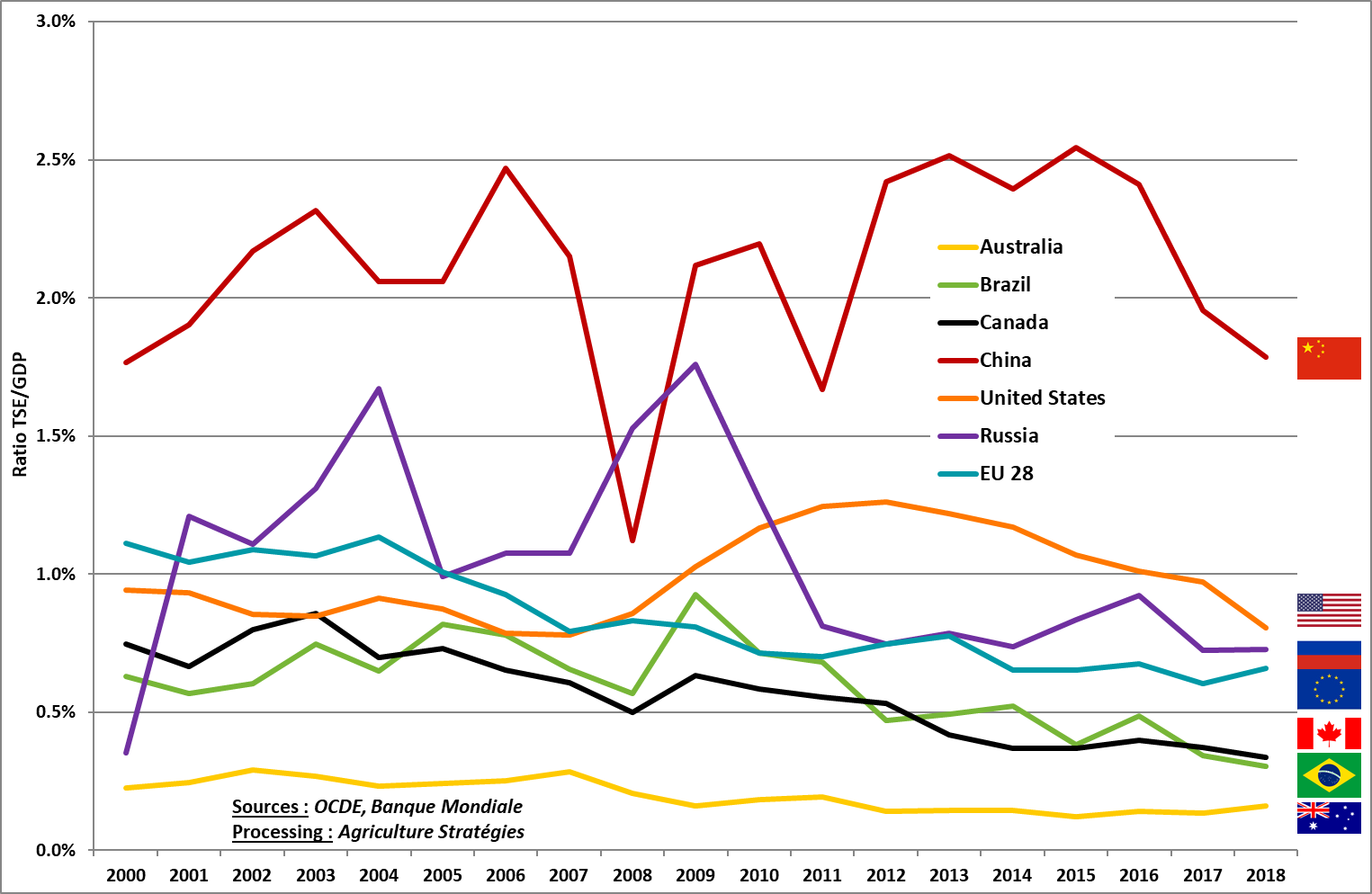

Figure 3 reports total support for country wealth as measured by gross domestic product (GDP). Figure 3: Change in the ratio of agricultural support to GDP for the main producing countries In terms of GDP, China is the country that spends the most support with the equivalent of 1.8% of its GDP. The decrease in 2008 corresponds to the rise in international prices: with China mainly supporting the protection of its domestic market, the gap between domestic and international prices has decreased significantly, thus lowering its TSE. Except for the fall of 2008, the ratio EST / GDP is relatively stable over the whole period even though China has experienced very significant growth. The Chinese development strategy has not gone through the sacrifice of its agriculture, a classic pattern of industrial development policies. On the contrary, the strengthening of China’s TSE is due to a concern to maintain a high level of food security while balancing the relationship between cities and the countryside and stimulating demand in the latter. The EU, which was in second place with around 1.1% in 2000, is now fourth with only the equivalent of 0.6% of GDP, overtaken by the United States and Russia. Brazil and Canada, with very different economies and levels of development, also experienced erosion of the same order of magnitude over the period to reach a TSE of 0.4% of GDP.

To get further into the analysis of the evolution of support, we are interested here in the estimation of producer support (PSE) that is related to the value of agricultural production (the turnover of the Agriculture). Figure 4: Ratio between PSE and total value of agricultural production for the main producing countries By comparing the PSE with the value of production, there is a convergence between developed countries (EU, US and Canada) where the ratio decreases, and emerging countries (Russia and China) where the ratio increases. These countries are in the range of 9.6% for Canada to 18.3% for the European Union. Australia and Brazil, however, remain away from this convergence with a producer support equivalent of between 3% and 4% of the total value of agricultural products.

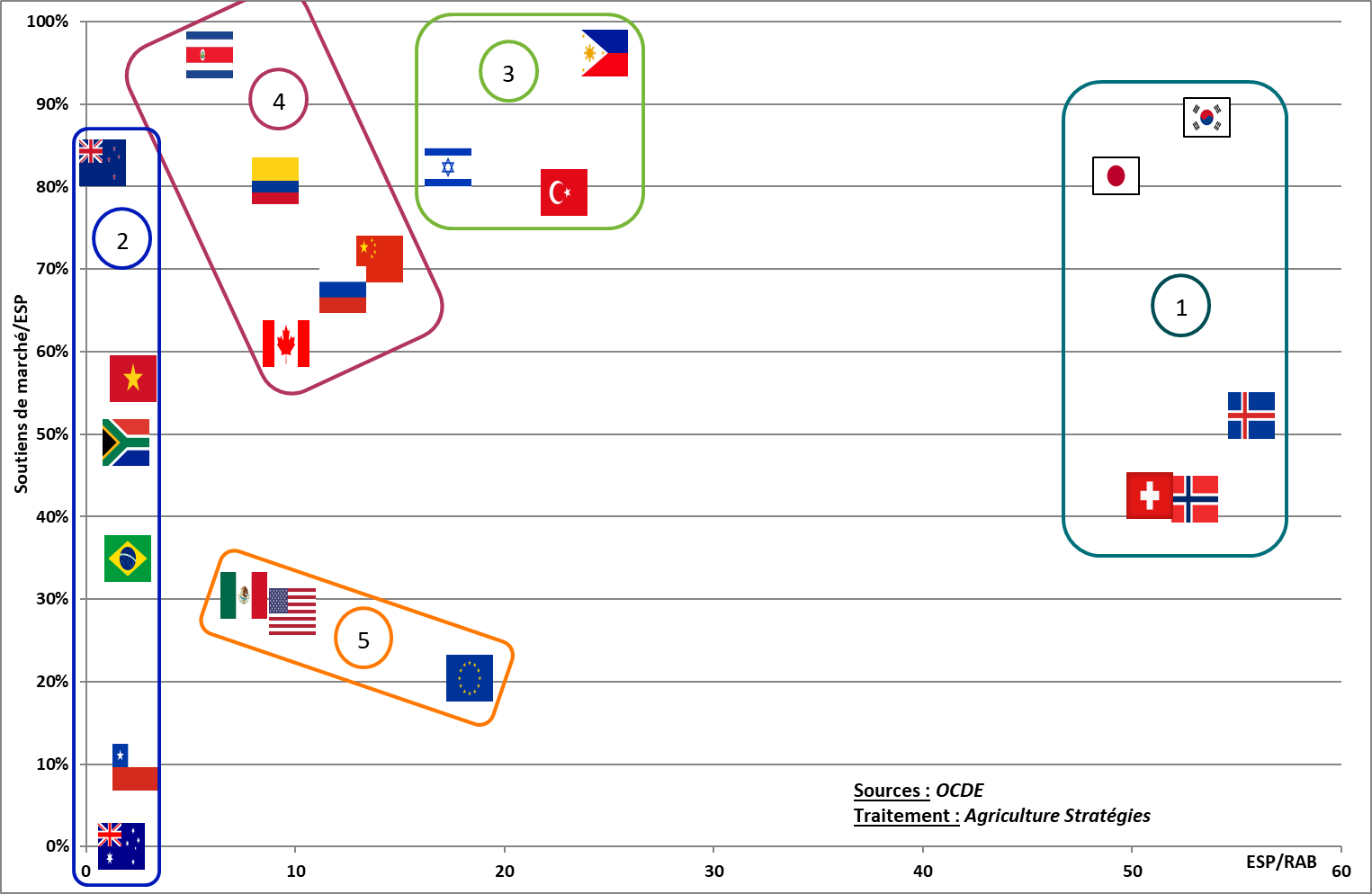

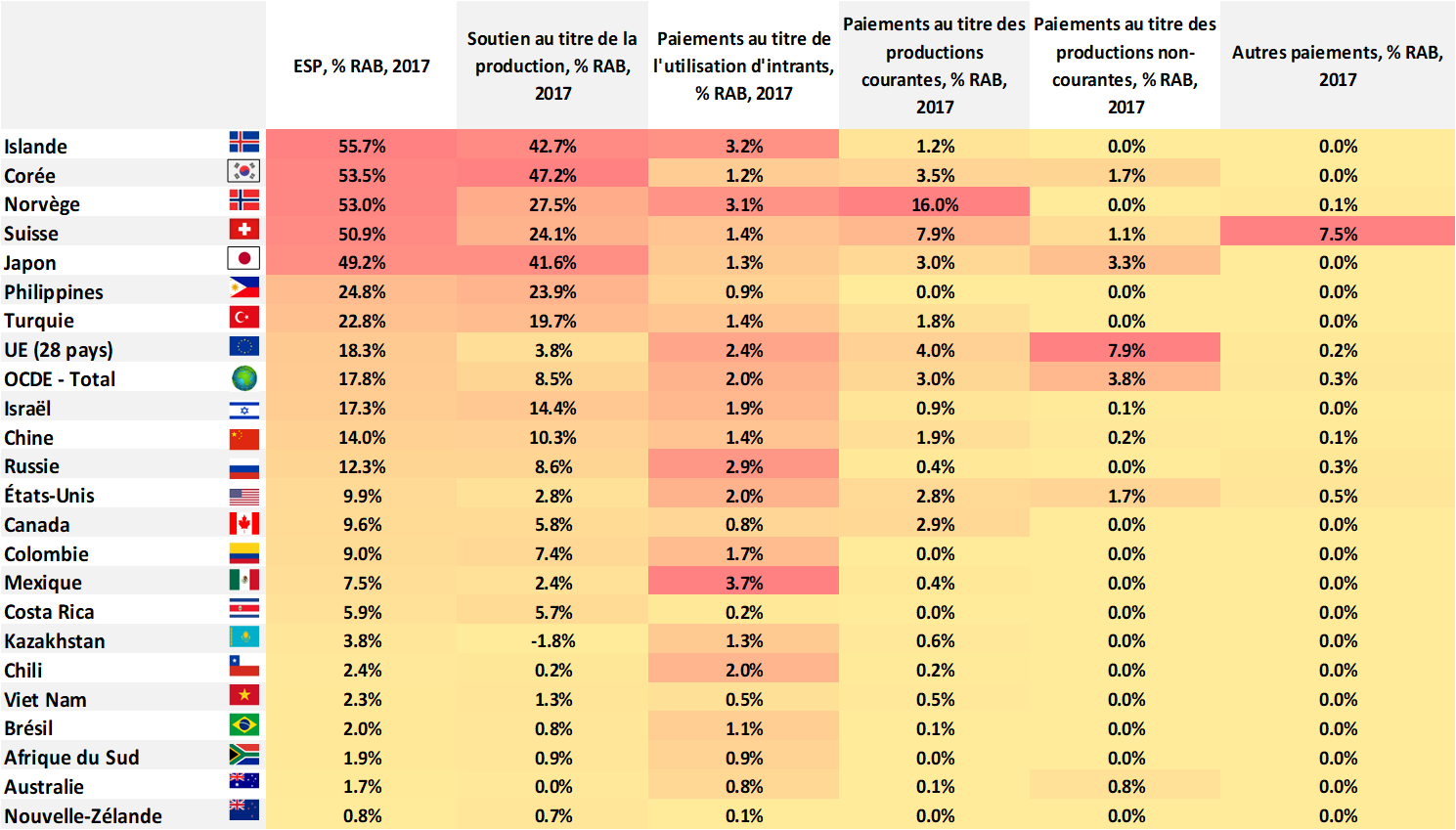

Beyond the top seven agricultural countries, the OECD is also the agricultural and food policies of other, less important countries in terms of production. The table below shows the PSE of each country and its components in relation to the value of production (RAB means Gross Agricultural Recipe) for the year 2017. The PSE is in fact broken down into 5 categories: output “corresponds to market support and thus to tariff protection,” input use payments “are direct aid for the purchase of inputs,” payments for current production ” are aid coupled with production volumes, “payments for non-current production” are decoupled and counter-cyclical direct aids established on a historical production reference, and finally the fifth category includes the other aids.  Figure 5: PSE and components of PSE relative to the value of agricultural products (OECD source) Figure 6 shows the great disparity in the level of PSE and its components relative to the value of agricultural products. For Japan, Switzerland, Norway, Korea and Iceland, producer support accounts for almost half of the value of the products. The Philippines and Turkey with 25% and 23% are above the EU (18%). At the other end, the value of the PSE for Ukraine is negative because of the fact that Ukrainian agricultural prices are lower than international prices, the difference being explained notably by the transport costs for exporting. New Zealand, Vietnam, Chile and Kazakhstan have a profile similar to Brazil and Australia previously seen. To go further, we are interested in the components of ESP. In the first place, it seems appropriate to isolate the support for production, which, it should be remembered, is not subsidies paid directly to producers, but support through customs duties which allow domestic prices to be above international prices. In Figure 7, we situate the countries according to two dimensions: in abscissa, the intensity of the ESP revealed via the ratio ESP / Gross agricultural receipts, and on the y-axis, the share of the market supports in the whole of ESP.

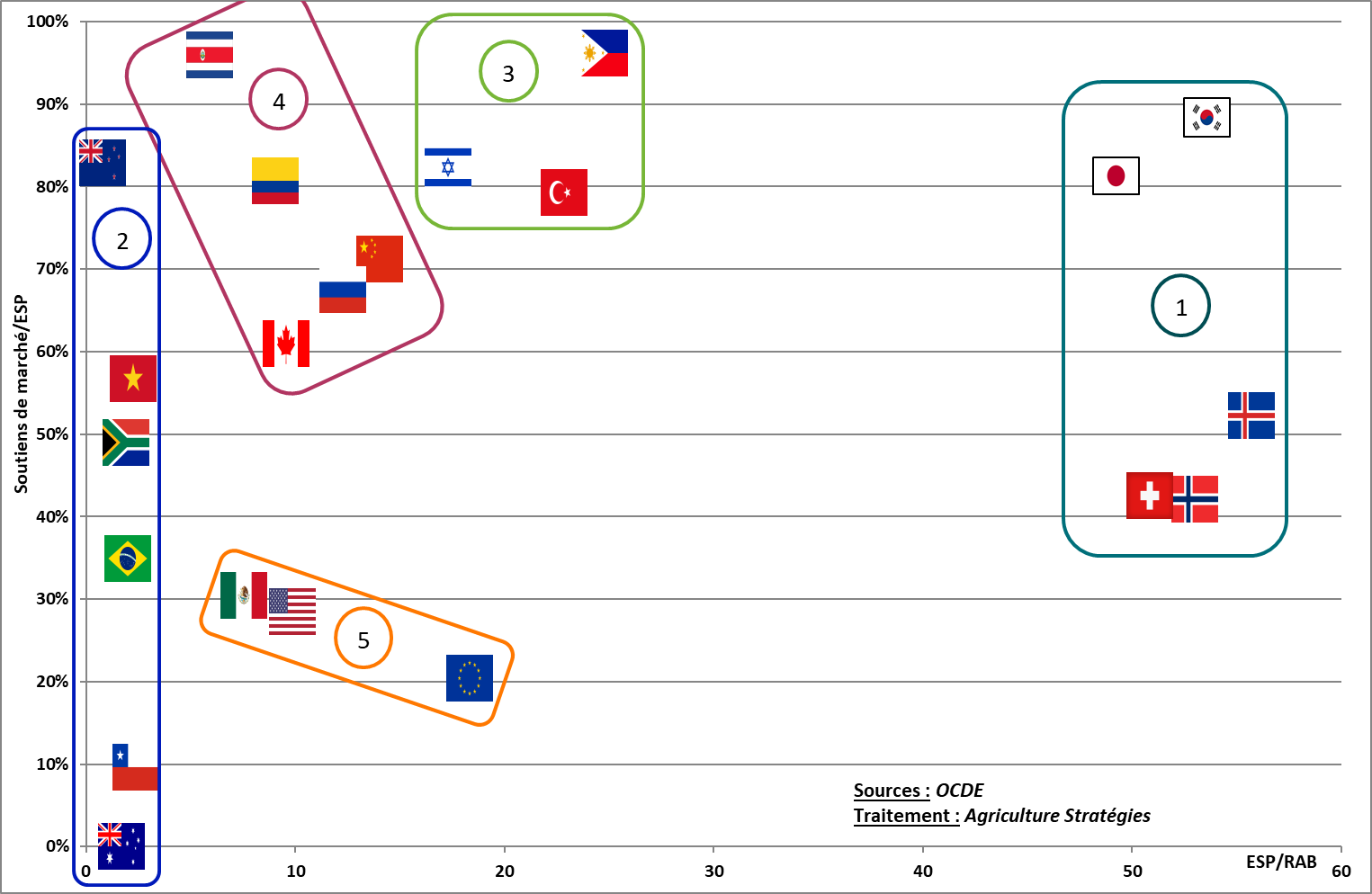

Figure 5: PSE and components of PSE relative to the value of agricultural products (OECD source) Figure 6 shows the great disparity in the level of PSE and its components relative to the value of agricultural products. For Japan, Switzerland, Norway, Korea and Iceland, producer support accounts for almost half of the value of the products. The Philippines and Turkey with 25% and 23% are above the EU (18%). At the other end, the value of the PSE for Ukraine is negative because of the fact that Ukrainian agricultural prices are lower than international prices, the difference being explained notably by the transport costs for exporting. New Zealand, Vietnam, Chile and Kazakhstan have a profile similar to Brazil and Australia previously seen. To go further, we are interested in the components of ESP. In the first place, it seems appropriate to isolate the support for production, which, it should be remembered, is not subsidies paid directly to producers, but support through customs duties which allow domestic prices to be above international prices. In Figure 7, we situate the countries according to two dimensions: in abscissa, the intensity of the ESP revealed via the ratio ESP / Gross agricultural receipts, and on the y-axis, the share of the market supports in the whole of ESP.  Figure 6: Typology based on the ratio ESP / Gross Farm Receipts and the share of market support in ESP The distinction made makes it possible to establish a typology where countries are divided into five groups:

Figure 6: Typology based on the ratio ESP / Gross Farm Receipts and the share of market support in ESP The distinction made makes it possible to establish a typology where countries are divided into five groups:

Although they share a small share of market support in the PSE, Group 5 is the most heterogeneous in that Mexico mainly mobilizes input subsidies, while the EU and the Member States United States uses the different categories and in particular that relating to “payments for non-current productions”. The latter includes counter-cyclical aid in the United States and decoupled aid for the European Union. These two types of aid have in common not to be based on actual production, but the former depend on the price level while the latter are paid regardless of any economic dimension.